Advanced negotiation strategy for high-stakes international business: managing power, risk, and complexity in global corporate deal-making

Authors

Paduraru Olga

Share

Annotation

The article discusses an in-depth negotiation strategy that makes it possible to successfully conclude international corporate transactions in conditions of "expensive capital", increased volatility and a complicated regulatory environment. The article emphasizes that the rising cost of borrowed resources and stricter requirements of investors and creditors are changing the logic of negotiations. Now, the key factors are not only the price and timing, but also the distribution of financial, legal and operational risks, the establishment of liability limits, termination conditions, performance guarantees and mechanisms for adapting the transaction to changes in external conditions. In addition, the multilevel nature of global transactions increases information asymmetry, increases the likelihood of delays, and requires management of an "operational closure model." Based on the generalization of modern approaches to the theory of negotiations, the article systematizes the instruments of contractual risk consolidation. This makes the outcome of the transaction more predictable and increases the stability of its legal structure.. The study drew important conclusions that in order to increase the effectiveness of negotiations and reduce the likelihood of transaction disruption, it is necessary to conduct risk-based training, standardize disclosures, and manage the approval process.

Keywords

Authors

Paduraru Olga

Share

Relevance of the study

The importance of this topic is due to the fact that today international corporate transactions are concluded in conditions of high capital costs, unstable markets and a complicated regulatory environment. The increase in the cost of borrowed resources and the tightening of the requirements of investors and creditors are changing the approach to negotiations. It becomes critically important for the parties to not only agree on the price and timing, but also to allocate financial, legal and operational risks, set limits of liability, determine the terms of termination, provide performance guarantees and provide mechanisms for adapting the transaction to changes in external conditions. As a result, negotiations go beyond tactical techniques and become a strategic management tool that directly affects the sustainability of corporate decisions and the economic impact of transformations.

Global transactions in the modern world are becoming more complex and multilevel. They involve several jurisdictions, regulators, stakeholders, as well as professional intermediaries and consultants. Because of this, it is becoming increasingly difficult to coordinate positions, and the information asymmetry is becoming more obvious. This increases the risk of delays or disruption of the transaction.

In such circumstances, a carefully developed negotiation strategy is of particular importance. It helps to control the positions of the parties, create coalitions of stakeholders, reduce transaction costs and find a balance between the speed of decision-making and the quality of legal and financial protection. Thus, the appeal to strategic negotiation management when concluding global corporate transactions is relevant and practice-oriented. It responds to the business's demand for reproducible methods that will help reduce uncertainty, protect the interests of the parties, and increase the predictability of results in an environment of high stakes, increased risks, and an increasingly complex architecture of international agreements.

The purpose of the study

The purpose of this study is to understand how the rising cost of capital and the increasing complexity of the institutional and regulatory environment affect the strategy of international corporate negotiations. We strive to systematize effective methods of managing conflicting interests of the parties, risks and multilevel complexity that arise when concluding large international transactions.

Materials and research methods

In the course of the research, we relied on modern negotiation theories, corporate risk management concepts, and generally accepted risk allocation tools within contracts, as well as open methodological and analytical materials that describe the practice of structuring transactions and decision-making in conditions of high uncertainty.

In the course of our work, we used various methods: theoretical analysis and generalization, comparative analysis of negotiation strategies, systematization of risks, as well as logical and structural analysis of multilevel factors and their impact on the negotiation process and the completion of the transaction.

The results of the study

In international business, negotiations are a complex process in which the parties seek to agree on the terms of the exchange, the distribution of risks and responsibilities. The success of these negotiations depends not only on the "price offer", but also on many other factors: the structure of the participants' interests, their alternatives, the institutional environment, cultural differences and dispute resolution procedures. The methodology of negotiation analysis in international business usually includes a combination of behavioral models that explain how parties make decisions and respond to pressure, economic and organizational approaches that describe the formation of a "pie of value" and its division, as well as legal frameworks that define the available enforcement and protection mechanisms in cross-border transactions.

In modern negotiation theory, it is customary to distinguish two strategies: "distributive" and "integrative". The first strategy focuses on the allocation of a fixed resource and the pursuit of one-sided gain, while the second is aimed at a joint search for options that will increase overall benefits and allow for better alignment of interests. The textbooks describe these strategies as two different sets of tactics and attitudes that affect the behavior of participants (for example, rigidity of positions, information exchange, attitudes towards trust and the duration of relationships) and the type of outcome (competitive "win-loss" or cooperative "win-win") [4].

An important part of the negotiation methodology is working with alternatives and the so-called "zone of possible agreement". This approach, which has become widespread in business practice and academic education, emphasizes that before starting negotiations, the best alternative to the BATNA agreement must be determined. It will become the minimum basis for decision-making. In addition, it is necessary to evaluate the ranges of possible concessions and their intersection (ZOPA). This will help you understand whether it is possible to reach a workable agreement and what conditions are within a reasonable compromise. The practical significance of these categories lies in the fact that they allow us to separate the "desirable" from the "acceptable". This reduces the risk of unfavorable concessions under pressure and allows you to more clearly justify your position in conditions where the stakes are high [6].

The model of "principled negotiations" occupies a special place in the negotiation process. It is based on separating people and problems, as well as focusing on interests rather than positions. Within the framework of this model, participants generate solutions and choose the best one based on objective criteria. This approach was described in a classic negotiation source and is widely used as a basic learning standard. It serves as a basis for discussing the terms of the deal, reducing the risk of mutual pressure and personal confrontation.

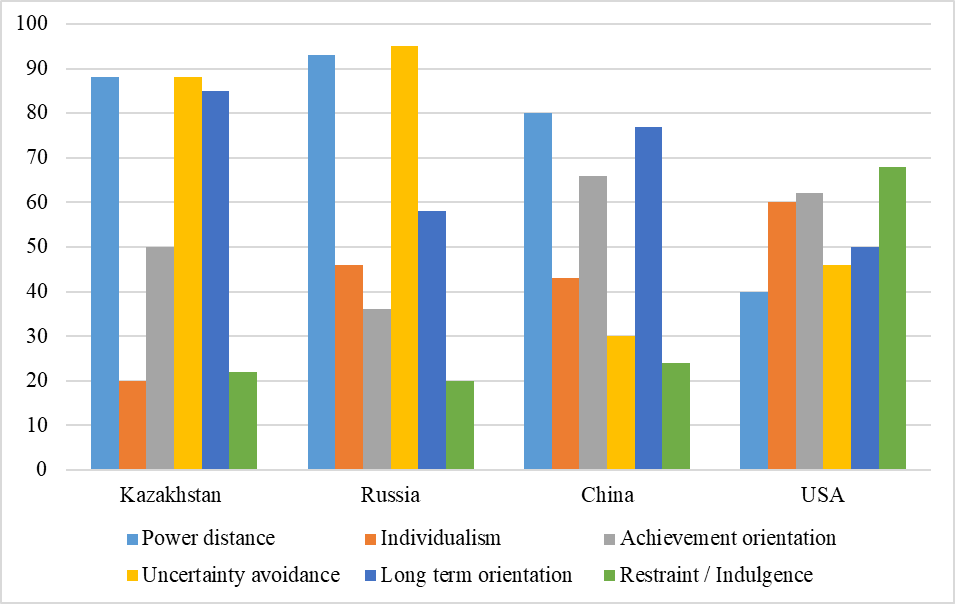

A special place in theory is occupied by cross-cultural approaches. This is due to the fact that international transactions take place in conditions of different approaches to hierarchy, individualism, uncertainty and long-term planning. Comparative cultural studies often use special measurements that make it possible to compare the "deep motives" of business behavior in different countries. Table 1 shows data on six such measurements for several countries. These data can be used as an empirical basis to explain differences in the negotiating style and expectations of the parties.

Fig. Comparative indicators of cultural measurements according to the Hofstede model for individual countries [1]

These indicators are not a direct prediction of the outcome of negotiations and cannot replace a detailed analysis of a specific transaction. However, they can be useful for forming hypotheses about possible preferences of the parties. For example, one can assume how natural rigid hierarchical communication will be, how directness will be perceived, how important formal procedures and detailed preparation are, as well as how orientation towards short-term results and willingness to invest in long-term relationships correlate.

In international negotiations, high interest rates are important not only as part of the overall macroeconomic context, but also as a factor that directly affects the cost of capital, yield requirements, and allowable debt burden. This, in turn, narrows or expands the possibilities for compromise on key terms of the deal. In a high-stakes environment, the parties re-evaluate time as a resource, distribute risks between price and contractual terms, and more closely link the outcome of negotiations with the availability of financing and the requirements of external participants such as banks, investors, and regulators. The policies of the largest central banks indicate that global markets are still operating in an environment of significant interest rates.

During the negotiation process, special attention is paid to reviewing the value of assets and changing the arguments related to the price. The expensive cost of capital makes cash flow forecasts more vulnerable to errors, so it is critically important to verify financial assumptions (through sensitivity analysis and stress scenarios). Negotiations are becoming contractual: the focus is shifting from general statements about future benefits to specific legal mechanisms that distribute risks and protect the parties in the event of a deterioration in external conditions. Analyzing the transaction market, it can be seen that in conditions of unstable inflation and interest rates, participants are more likely to adjust the structure of transactions and increase the requirements for legal certainty and risk management.

Another way to influence negotiations is through changes in the financing discussion. As debt, servicing becomes more expensive, the importance of conditions related to debt obligations, covenants, and "financing as a condition for closing a deal" increases. This leads to a redistribution of forces: a party that controls access to capital or is able to close a deal without expensive debt gets more opportunities to set its own terms. And a party that depends on external financing is forced to compensate for the risks of the other party, with either price, guarantees, or a payment structure.

Due to the high cost of capital, negotiations are increasingly shifting the focus from discussing a single price to discussing how to distribute uncertainty over time. In practice, this is reflected in the increased use of deferred payments and conditional price elements, such as earn-out, as well as in the growing interest in instruments that partially replace external debt, such as vendor loans. Industry reviews of the terms of transactions directly indicate an increase in the use of earn-out and more frequent access to vendor loans against the background of the high cost of external debt financing (Table 1).

Table 1

Changes in the applied pricing and financing mechanisms in M&A transactions in conditions of high debt cost

|

Mechanism |

Why is it becoming more in demand at high rates |

A typical negotiation conflict over the mechanism |

|

Earn-out |

Reduces the risk of overpayment in the absence of accurate forecasts and transfers part of the cost for the period after closing. |

Metrics and calculation period; post-closure management control; acceleration/early payment rules.

|

|

Vendor loan |

Partially compensates for expensive external debt and helps to eliminate the difference between the expected and actual cost. |

Percentage/ collateral/ subordination; default triggers; priority of requirements.

|

|

Deferred payment |

Provides the customer with liquidity and strengthens the financial structure. |

Guarantees and collateral; conditions of early recovery; connection with violation of the terms.

|

|

Enhanced guarantees and assurances |

They help to compensate for the increased likelihood of negative scenarios and increase confidence in the deal. |

Limits of liability; disclosures; exclusions; duration and procedure for filing claims.

|

A source: author's development based on [2].

In conclusion, in a high-stakes environment, time and regulatory predictability are of particular importance. This leads to the fact that in negotiations it becomes increasingly important to agree on conditions that allow you to control the process: deadlines, closing conditions, grounds for termination of the transaction, as well as the distribution of regulatory and possible delays. According to M&A market experts, in light of changes in the macroeconomic environment and the regulatory agenda, companies and investors are paying more and more attention to the legal conditions and structure that ensure the successful completion of the transaction and allow effective risk management.

In international corporate negotiations, risk management is carried out in accordance with the approaches adopted in the field of management and audit. In these disciplines, risk is seen as an integral part of strategy, closely related to business goals. It affects decision-making, control over their execution, and the quality of information disclosure to management. Negotiations in this context turn into a process of transforming identified risks into legally established mechanisms. What cannot be reliably reduced through organizational measures is fixed in the transaction structure, closing conditions, allocation of responsibilities, and dispute resolution procedures.

In real practice, risk-based negotiations begin by dividing a transaction into separate verifiable blocks. These blocks include commercial assumptions, the legal status of assets, regulatory restrictions, sanctions and compliance factors, as well as operational dependencies and execution risks. Then the parties agree on which risks are critical for closing the transaction, and which can be compensated or taken into account in control procedures. In conditions of uncertainty, the unified clauses on force majeure and significant change of circumstances developed by the International Chamber of Commerce (ICC) are of particular importance. These clauses increase legal certainty and determine in advance the consequences of obstacles or changes in the terms of the contract.

To demonstrate how risks are transformed into contractual decisions, table 2 below shows the main risk management tools in an international transaction and their purpose.

Table 2

Contractual risk management tools in an international transaction and their purpose

|

Instrument |

What risk do we exclude |

What exactly is agreed upon in the negotiations |

|

Representations, Warranties, and Disclosures |

There is a risk of receiving false information about the purpose of the transaction and assets.

|

The scope of guarantees provided, exceptions to them, standards of knowledge, the procedure and format of information disclosure. |

|

Closing Conditions and Preliminary Covenants |

There is a risk that the company will not be able to complete its operations due to regulatory requirements, lack of financing, or the need to obtain corporate permits. |

A list of conditions, the procedure for their fulfillment, deadlines and possible consequences of non-compliance. |

|

Limitation of Liability and Indemnification Procedures |

The risk of unforeseen financial losses. |

Limits, deductibles, time limits for filing a claim, and the procedure for calculating damages. |

|

Retentions/Securities of Performance (Including through Escrow) |

There is a risk that the obligations will not be fulfilled after the closure.

|

The amount of the deduction; the events that serve as the basis for the write-off; the procedure for resolving possible disagreements. |

|

Force Majeure and Hardship Clauses (ICC) |

The risk of non-fulfillment of obligations or significant changes in the situation.

|

Criteria for the event, notification, consequences, possibility of revision or termination. |

A source: author's development based on [3].

Global corporate transactions are a complex process that includes several aspects: commercial, financial, legal and regulatory. Even if the parties reach an agreement on the price and the basic ownership structure, the result depends on external control procedures, which have their own deadlines, criteria and disclosure requirements. Complexity management in the negotiation process implies control over a multi-level system of approvals and the creation of a contractual structure that will be feasible and economically justified, despite possible delays, regulatory conditions and the need for adjustments.

The main reason for the multilevel is related to antitrust control and inspections of foreign investments for national security, especially when it comes to cross-border transactions. These regimes significantly expand the agenda of negotiations: the parties need to agree in advance on a list of permits and notifications, assign responsibilities for the preparation of materials, and determine the consequences of possible delays, terms of closing the transaction and rules of conduct in case of conditional approval or requirements of the regulatory authority [5].

As a result, the "operational closure model" becomes the main tool that allows you to manage the complexity of the process. It determines who interacts with regulators and how, what risks are considered critical, what measures are acceptable to obtain approval, how costs and responsibilities are distributed, and what exit rights are provided in case of an adverse development. The multi-stakeholder composition of the process, including creditors, consultants, auditors, and other stakeholders, further complicates the situation. That is why a single communication channel, data discipline, and consistent document control and disclosure procedures are critically important.

The development of a deep negotiation strategy in international corporate transactions implies a transition from situational decisions to a well-thought-out model in which economic conditions, legal mechanisms and the management process are interconnected. Efficiency is achieved through a clear statement of goals and constraints at the preparation stage. The subject of negotiations usually includes not only the price, but also the procedure for closing the transaction, the distribution of risks, requirements for compliance with legislation and the consequences of possible adverse events. The strategy should take into account the interests of the parties and acceptable concessions, as well as include specific contractual instruments. This will minimize the likelihood of future disputes.

The effectiveness of negotiations increases due to the fact that the information preparation and management process is standardized. This implies the use of uniform source data, clear rules for information disclosure, as well as the establishment of an agreed communication channel and version control of documents. A risk-based approach is an important aspect of negotiations. It involves ranking risks according to their degree of criticality and consolidating them through closing conditions, obligations of the parties, limitations of liability and dispute resolution procedures. In addition, the effectiveness of negotiations is significantly improved due to a clear distribution of roles in the team, the discipline of agreeing on concessions and the predictability of interaction. These factors contribute to building trust between the parties and speeding up the process of reaching an agreement.

Conclusions

Thus, in conditions of high capital costs and a volatile external environment, international corporate transactions become a strategic management tool. The key factors in such negotiations are the distribution of risks and the legal certainty of the terms. The effectiveness of negotiations is significantly enhanced by a risk-based approach. It involves dividing the transaction into verifiable blocks, identifying critical risks for its completion and consolidating them in the form of representations and guarantees, closing conditions, limitations of liability, security mechanisms and agreed procedures in case of obstacles or significant changes in circumstances. The multilevel nature of global transactions requires a managed "operational closure model" and coordination with regulators and other stakeholders. Standardization of training, information management, and decision-making discipline reduce transaction costs, build trust, and increase the predictability of negotiation outcomes.

References:

- Country comparison tool [Electronic resource]. – Access mode: https://www.theculturefactor.com/country-comparison-tool.

- Deal Terms Report 2025: European Market [Electronic resource]. – Access mode: https://www.dealsuite.com/fr/blogs/m-a-deal-terms-report-2025-european-market.

- ICC FORCE MAJEURE AND HARDSHIP CLAUSES [Electronic resource]. – Access mode: https://iccwbo.org/wp-content/uploads/sites/3/2020/03/icc-forcemajeure-hardship-clauses-march2020.pdf.

- Negotiation web [Electronic resource]. – Access mode: https://assets.publishing.service.gov.uk/media/57a08b4540f0b652dd000bca/Negotiationweb.pdf.

- REGULATION (EU) 2019/452 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL [Electronic resource]. – Access mode: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX%3A32019R0452.

- Sucuri WebSite Firewall – Access Denied [Electronic resource]. – Access mode: https://www.pon.harvard.edu/.

Other articles of the issue